Welcome Back to Pullman

The hyperscalers arebuilding their own power plants: restarted reactors, contracted small modular nuclear, gigawatt-scale behind-the-meter gas. The last time American industrialists tried to own the utility stack, it led to monopolies. Are we repeating history?

In 1880, a man named George Pullman bought a stretch of prairie thirteen miles south of Chicago and built a town on it. Not a town in the sense of a place people chose to live - a town as a piece of industrial infrastructure for a single company. Pullman's Palace Car Company manufactured the luxury sleeping cars that defined American long-distance rail travel, and Pullman had decided that the workforce, the housing, the gas works, the water plant, the library, the church, the bank, the school, and the hotel would all be owned by the company. There would be no saloons. The streets would be cleaned by Pullman employees. The rents would be paid to Pullman. The gas in the lamps would be generated by a Pullman plant and metered through a Pullman pipe.

By 1885 Pullman had twelve thousand residents living inside this experiment. The model was so admired internationally that it won the Grand Prize at the 1896 International Hygienic and Pharmaceutical Exposition as the most perfect industrial town in the world.

Thirteen years after he built it, Pullman didn't own any of it. The Illinois Supreme Court ordered him to divest the entire town in 1898, ruling that the ownership of a complete civic infrastructure by a private manufacturing corporation was "incompatible with the theory and spirit of our institutions." Pullman had to sell every building that wasn't directly part of railcar production. The gas works went. The water plant went. The houses went onto the open market. The vertical integration that had produced the most admired industrial site of the 1890s lasted not quite one full business cycle.

The American hyperscaler industry is in the middle of trying to build it again.

The grid fight had a second act nobody was watching for

I have written a lot about the front of the grid fight. "The Grid Said No" covered the 11 GW of announced data center capacity sitting frozen because regional grid operators cannot deliver the interconnect on the calendar the financial models assumed. "The Permission Problem" covered the political-economy reversal in Loudoun County and the cascade of moratoriums it set off across thirty states. Both pieces ended at roughly the same observation: the binding constraint on the buildout is no longer technical. It is the willingness of a county commissioner, a state utility regulator, or a regional transmission organization to let you turn the racks on in the year you need them turned on.

What I underweighted in both pieces was the response.

Faced with a public grid that has discovered it can say no, the four largest hyperscalers spent 2024 and 2025 signing deals that look - when you stack them in one place - like the largest private utility buildout in American history. Microsoft signed a twenty-year purchase agreement with Constellation Energy to restart Three Mile Island Unit 1, the reactor that had been mothballed since 2019, dedicating the entire 835 MW output to a single corporate customer. Amazon Web Services bought Talen Energy's Cumulus campus sitting next to the Susquehanna nuclear plant, a $650 million deal for 960 MW of direct nuclear feed without ever touching the regional transmission grid. Google signed a 500 MW commitment with Kairos Power for the first commercial fleet of small modular reactors. Meta signed PPAs across four states for new natural gas turbine capacity dedicated entirely to single-campus loads. xAI installed thirty-five gas turbines on a single Memphis site - initially without air permits - to bring a frontier-scale training cluster online in months instead of the years a grid-tied build would have required.

The combined nameplate capacity sitting under these deals is somewhere north of 10 gigawatts of dedicated, single-customer generation, a footprint roughly the size of the nuclear fleet of France. None of it is on the public grid in the sense the public grid was designed for. The hyperscalers are not buying power from the utility. They are becoming the utility, and they are doing it on a calendar that the public utility cannot match.

The trade looks clean on a deal memo. The grid won't serve you for five years; you can have a dedicated reactor restart in two and a half. The substation queue is forty-eight months; the gas turbine vendor will ship in nine. Behind-the-meter generation moves you out of the queue you were losing and into a queue you can pay to skip. Every CFO presentation I have seen on this in the last six months treats the math as obvious.

The math is obvious. The thing the math omits is the part that matters.

What the deal memo does not say

When a manufacturing company owns the generation stack underneath its production sites, three things happen that do not happen when it buys the same power off the grid, and all three are showing up in the hyperscaler buildout right now.

The first is regulatory exposure. A regional utility builds a generation asset under a rate case approved by a state public service commission, and the rate-base recovery model spreads the cost and the regulatory risk across millions of customers. When Microsoft restarts Three Mile Island for itself, the rate case becomes a single-counterparty contract subject to whatever rules the NRC, FERC, and the relevant state commission decide to impose this decade. The rules are not stable. Pennsylvania, New Jersey, and Ohio have all introduced legislation in the last six months to either tax behind-the-meter loads at the same rate as transmission-level loads or to require dedicated generation deals to include a public-benefit contribution. None of those rules existed when the deals were signed. All of them are now real liabilities on the corporate balance sheet of the buyer, not socialized across a ratepayer class.

The second is operational complexity. A hyperscaler's data center operations team is, structurally, a software organization. It is extremely good at running fleets of homogenous compute, at automating failure recovery, at managing complex but well-understood control loops. It is not, by training, an operator of nuclear plants, gas turbines, or grid-scale battery installations. Talent for those roles does not transfer from the data center side; it transfers from the utility side, which has been shedding skilled operators for two decades and is itself short. The hyperscalers are now hiring across that gap, and they are hiring at a price that is starting to show up in the cost basis of the same regional utilities they bypassed. The labor market for a senior reactor operator is, as of this quarter, structurally tighter than the labor market for a senior site reliability engineer. That cost is not going down.

The third is political-economy exposure. The original argument for socializing grid investment was that the utility, as a regulated monopoly, absorbed the externalities - the emissions accounting, the water consumption, the noise complaints, the community impact - under a public framework with a public hearing. When the hyperscaler builds its own generation, those externalities do not vanish. They move onto the hyperscaler's site, the hyperscaler's environmental report, and the hyperscaler's PR budget. The Memphis turbines are the first version of this story to break into the national press. They will not be the last. The same county commissioners who discovered they could say no to a hyperscale campus will discover, on the same calendar, that they can say no to a hyperscale gas plant. Building your own generation does not exempt you from the political fight over generation; it makes you the protagonist of it.

This is the part the Pullman story actually rhymes with. Pullman did not lose the town because the gas works failed or because the houses were poorly built. He lost it because the act of owning the full vertical stack put him in a political relationship with the public that the public eventually refused to accept. Owning a town meant being the landlord during the recession, the wage-setter during the strike, and the rent-collector during the federal intervention. The vertical integration that looked like a moat in 1885 was a target by 1894. The hyperscalers are not in 1885. They are somewhere around 1892.

The architecture has a different answer

The reason this matters for the larger argument I keep making is that there is a perfectly good alternative, and it is the alternative this site has been pointing at for two years.

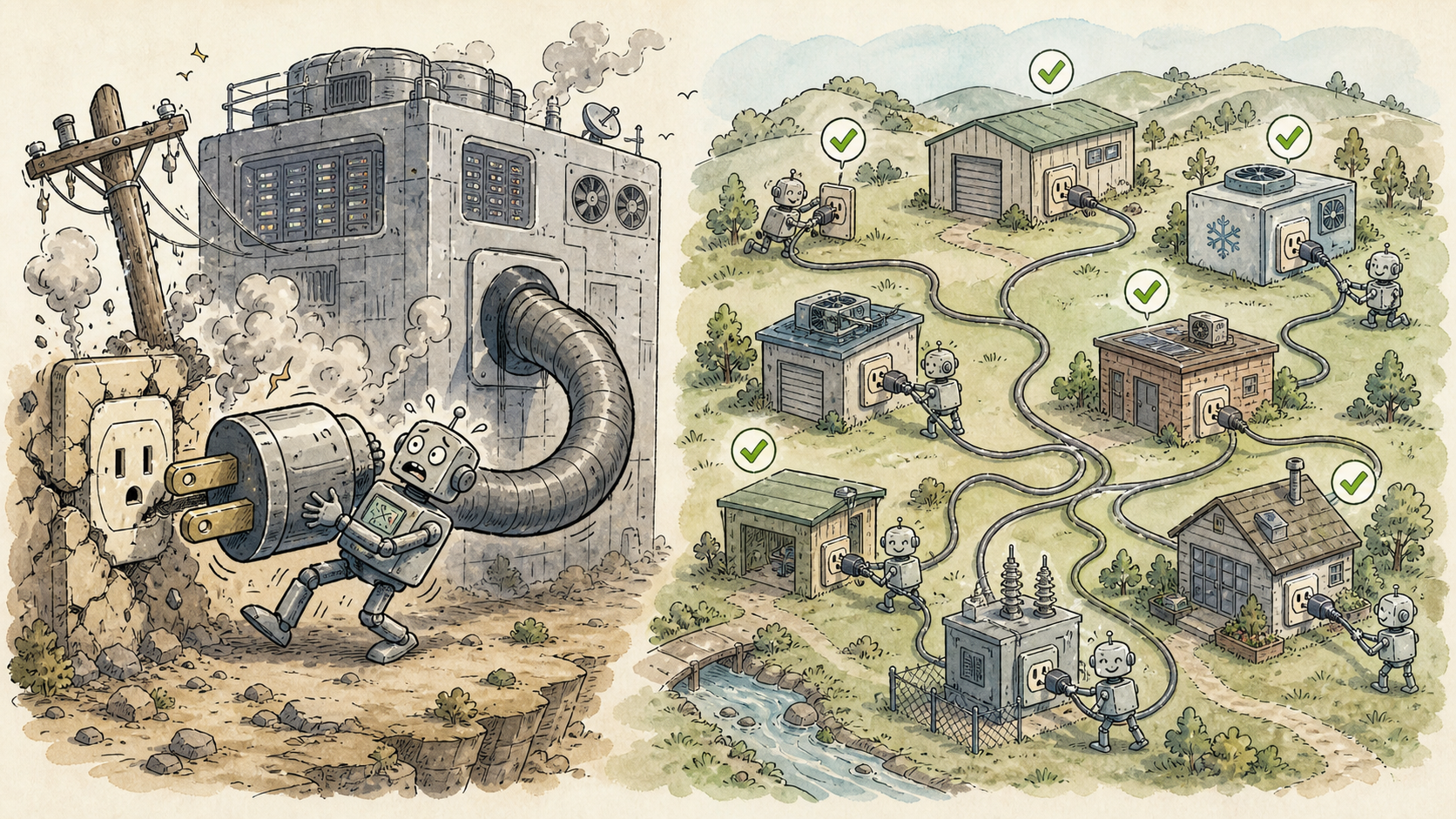

A 2 GW campus needs 2 GW of dedicated generation. It needs that generation in a single place, with single-site permitting, single-site water, and single-site political risk. A workload that is the same size, distributed across 200 sites at 10 MW each, needs 10 MW of generation per site. Ten megawatts is a load profile that the existing grid can absorb almost everywhere in North America without a substation upgrade, without a behind-the-meter generation deal, and without becoming the protagonist of a county commission meeting. Ten megawatts is the load of a mid-sized cold-storage facility. Nobody fights about cold-storage facilities.

This is not a marketing line. It is a thermodynamic property of the buildout. The reason the grid is fighting back, and the reason the hyperscalers are now reaching for the utility stack underneath them, is that hyperscale-class concentration of compute requires hyperscale-class concentration of power. Distribute the compute and the power problem decomposes into a series of problems each of which the existing system already knows how to solve. Concentrate the compute and the power problem aggregates into a single problem the existing system was specifically built not to solve at that scale.

The hyperscalers are picking the harder path because the inference inversion has not fully landed in their capex committees yet. The CFO calendar still treats a 2 GW campus as the unit of account. Until it stops treating it that way, the response to a hostile grid will continue to be vertical integration, and the response to vertical integration will be - on a delay of a few years, but reliably - the same response the Illinois Supreme Court gave Pullman. There is a part of the public infrastructure that the public will not let a single counterparty own outright, and electrical generation has been on that list for the better part of a century. The deals being signed this quarter are an argument that the list has changed. The political response over the next thirty-six months will determine whether the argument holds.

My bet is that it does not. Pullman did not lose because the buildout failed; the buildout was magnificent. He lost because the buildout produced a relationship between the company and the public that the public eventually voted against. That vote, in 2026, looks like a state legislature passing a behind-the-meter surcharge bill. It looks like a public service commission requiring single-counterparty generation deals to include rate-payer subsidies. It looks like a federal rule from the Treasury or the EPA changing the tax treatment of dedicated nuclear restarts. None of these are speculative. All of them are on legislative calendars right now, in jurisdictions where the same fight that produced the moratoriums in Loudoun produced the bills.

The hyperscaler answer to "the grid said no" was to build the grid themselves. The historical track record on that move, in the United States, is not encouraging. The thing that ended Pullman was not the depression of 1893. It was the discovery, by everyone outside the company, that the company had built something it was not entitled to keep.

Financing a 2 GW behind-the-meter buildout COULD work. But financing a buildout that does not require it would be even better.

Want to learn how intelligent data pipelines can reduce your AI costs? Check out Expanso. Or don't. Who am I to tell you what to do.*

NOTE: I'm currently writing a book based on what I have seen about the real-world challenges of data preparation for machine learning, focusing on operational, compliance, and cost. I'd love to hear your thoughts!